Global Elevator Industry Becoming Increasingly Service-Driven

Global Elevator Industry Becoming Increasingly Service-Driven

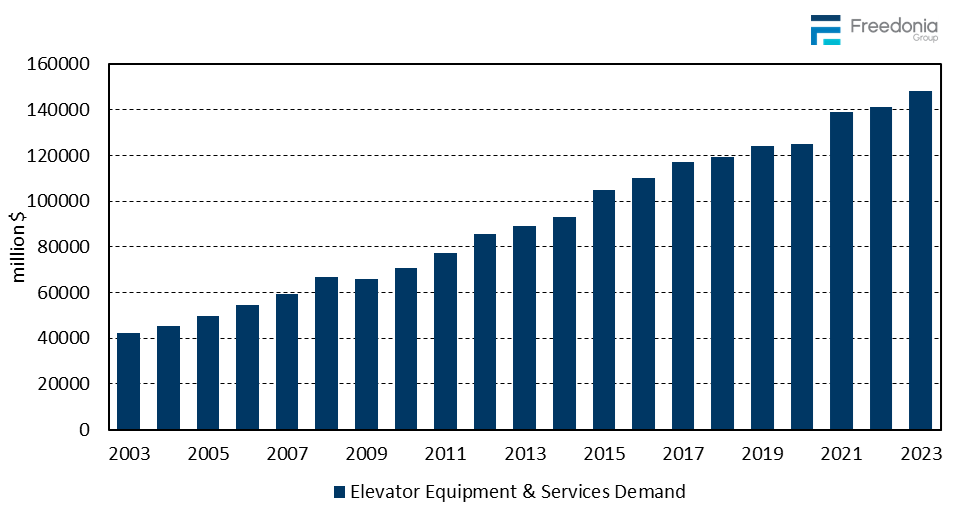

As of 2023, services accounted for a slightly greater share of global elevator industry revenues, a trend that began during the middle part of the previous decade. Stronger growth for services is expected to continue going forward, and industry leaders are increasingly emphasizing the development of their service businesses. Growth in service revenues reflects the ongoing expansion of the global elevator stock, which will require continued spending on maintenance alongside periodic large expenditures for more extensive modernization.

As of 2023, the share of the global elevator stock that was over 20 years old was estimated at around one-third. Throughout the ensuing decade, many units that were installed from 2000 to 2010 will reach ages where significant modernization is required. Rising services spending will likely continue into the 2030s, reflecting the especially high levels of new elevator installation in industrializing countries seen during the 2010s.

China Services Market Represents Key Area of Focus

While China was by far the world’s largest national market for elevator equipment and services in 2023, the country’s new installations market no longer represents a strong growth area. With the maturation of China’s building construction industries, new elevator installations in the country peaked in 2017 and are not expected to reach this level again in the near future.

However, the massive number of elevators installed in China during the country’s 21st century building boom reflects potential for significant growth in services demand going forward as the installed stock ages. As a result, global market leaders are increasingly focusing on China’s service market as a driver of revenue gains going forward.

Production Patterns Driving Geographic Diversification

While international trade in elevator equipment is substantial, most global demand needs are met by local production, with on average over 80% of output by value used in its country of origin. When developing new geographic markets, multinational producers are heavily incentivized to establish local production, reflecting both high transportation costs and the need to collaborate closely with clients.

Going forward, many of the world’s fastest growing elevator markets are expected to be industrializing countries in the Asia/Pacific and Africa/Mideast regions that are not yet major national markets. To properly serve these markets, multinational producers will need to emphasize developing local production bases, either through wholly new operations or via the acquisition of smaller local firms.

Historical Market Trends & Growth Factors

Global demand for elevators is shaped by a variety of factors, with considerable variation on key factors depending on region and country. The industry is primarily driven by trends in urban development, construction activity, and demographic shifts, but several other forces also play a role. Specific factors impacting the market include:

- Urbanization & Population Growth: Rapid urbanization, particularly in emerging markets, drives demand for new elevators in both residential and commercial buildings.

- Economic Cycles: Overall demand fluctuates with economic conditions, as slowdowns in construction reduce elevator installations, while growth periods boost demand.

- Construction Activity: High-rise construction and infrastructure development in both developed and developing regions boost demand for elevators in new buildings.

- Aging Infrastructure, Modernization & Retrofits: Aging building infrastructure, particularly in developed countries, increases demand for upgrading or replacing older elevator systems.

- Aging Population: In countries with aging populations, demand rises for elevators in residential settings, retrofits, and accessibility projects.

- Technological Advancements: Smart, energy-efficient, and space-saving elevator solutions create new opportunities for sales, particularly in premium building projects.

- Regulatory Requirements: Safety and environmental regulations drive both new installations and upgrades, especially in densely populated urban areas.

- Sustainability Trends: Green building certifications and environmental initiatives encourage the adoption of energy-efficient elevator systems.

Elevator Equipment & Services Demand by Market

Elevators and related products and services are utilized in a broad array of structures featuring multiple floors or levels, as well as in certain single-floor facilities. Large, well-trafficked buildings with multiple stories – such as office buildings, institutional buildings, and transit stations – tend to be the most intensive users of elevator products and services.

In Western Europe and parts of Asia where urban, multifamily housing is more common, the residential market is particularly important, accounting for the majority of demand in some countries. At the higher end, single-family homes have emerged as a niche elevator market that will support demand in high-income countries with aging populations, such as Japan. Nevertheless, this segment is likely to remain only a tiny portion of the elevator market for the foreseeable future.

For escalators and moving walkways, the key users are large retail venues, such as shopping malls, sports stadiums, and transportation venues, such as airports and subway stations. These applications require the rapid movement of a large volume of people either between levels or across rather large distances.

Pricing Trends

Numerous factors impact the price of a new elevator unit:

- Elevators with larger cabs are more costly because they require more materials to construct and must use stronger and more powerful lifting components.

- Elevators with greater travel distances require more materials for the lifting components, and, more importantly, require more advanced technologies to improve the ride, safety, and integration into the building overall.

- Nonresidential units tend to be larger and require more durable components, as they typically see more intensive use and are often exposed to the elements in the case of stadiums or metro systems; moreover, regulations for nonresidential buildings tend to be more stringent.

- Prices are also affected by local manufacturing costs and exchange rates, but competition from imports in a country tempers this somewhat, as elevators are generally priced on the world market.

North America has the highest average elevator prices, driven by accessibility regulations that drive the use of larger elevators as well as the high share of the market held by nonresidential elevators. In comparison, Western Europe, which has by far the highest share of demand in the residential market of any world region, has much lower prices, as elevators used in the region tend to be significantly smaller than those in North America.

The Asia/Pacific and Africa/Mideast regions have the lowest average prices per unit due to regulations that may be less strictly enforced as well as a lower standard of living that allows building owners to forgo premium features such as more expensive cab and door finishes, high-speed models, or energy saving technology.

In the 2018-2023 period, several factors affected the pricing growth of new passenger and freight elevators:

- Especially high inflation in years impacted by the COVID-19 pandemic drove prices upward, as illustrated by the rapid pricing growth seen in North America between 2018 and 2023.

- However, the strengthening of the US dollar reduced global average prices denominated in dollar terms over this same span.

- Taken together, the impact of these trends balanced out to an extent over the 2018-2023 period.

Going forward, materials and labor cost inflation are expected to moderate to rates more typical of recent historical eras as the pandemic-driven high-inflation period ends. More widespread deployment of value-added features will also contribute to pricing growth, while tighter regulation will serve to boost prices in the Asia/Pacific region.

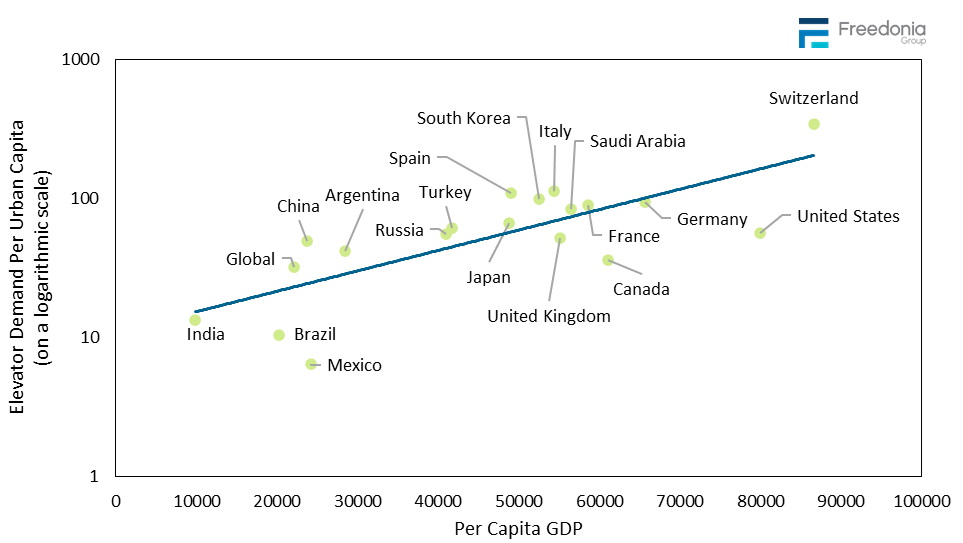

Relationship of Per Capita Income & Elevator Demand

Demand for elevator equipment and services in an individual country generally grows with the income of its residents:

- All else being equal, a country with a higher average per capita income will also have a higher level of elevator equipment and services demand per urban resident.

- While factors such as the nation’s distribution of wealth can also come into play, per capita GDP is a consistent and widely available proxy for a nation’s standard of living.

Demand for elevator equipment and services is measured relative to a country’s number of urban residents instead of total population to control for differences in urbanization across different markets. If two countries have similar total populations and per capita GDPs but one is more urbanized, the more urbanized country will likely have higher demand for elevator equipment and services because it will likely have more tall buildings.

The following chart illustrates how demand for elevator equipment and services varies with per capita income. The solid line represents the estimated relationship of elevator demand per urban resident relative to per capita GDP.

Divergences from the estimated relations occur for a variety of idiosyncratic reasons, including the composition of the economy, prevalence of mid- and high-rise buildings, and population density. For example, elevator demand per urban resident is higher in Japan than in Canada despite higher income levels in Canada because Japan is far more densely populated, making high-rise buildings more common.

Report Details

This study analyzes the global market for elevators (including passenger and freight elevators), escalators, and moving walkways; and associated parts that are sold separately, such as controls, doors, sensors, and power transmission equipment. This study also covers demand for installation services and modernization services.

- Elevators are vertically moving platforms enclosed in a shaft, used to transport passengers or goods between different floors of a building. Controlled by mechanical systems, they rely on motors and cables or hydraulic mechanisms. Elevators are integral to high-rise buildings, enabling efficient vertical transportation.

- Escalators are motorized, continuously moving staircases that transport people between floors. They are often found in public spaces like malls, airports, and transit stations, providing convenient access without the need for stairs or elevators.

- Moving walkways (also called travelators) are flat or slightly inclined conveyor systems used to transport people horizontally or on gentle inclines over short distances. Common in airports and large commercial areas, they allow people to stand or walk, speeding up movement over long hallways.

For the purposes of this study, general references to elevators or the elevator market include escalators and moving walkways, parts, and services, while elevators themselves, often referred to as lifts in European publications, are described as passenger and freight elevators.

Historical data (2013, 2018, 2023) and forecasts to 2028 and 2033 are presented in dollars. Annual data for 2020-2027 are also presented. Passenger and freight elevator stock and demand are presented in units.

Products beyond the scope of this study include aerial work platforms (man lifts), chair lifts, and conveyor systems used for the transport of goods.